Cost

The effect of energy-saving measures on the housing costs of the tenants was determined. These costs relate both to the energy bill for the tenants and to the level of the rent after renovation.

The proposed renovation measures will ultimately result in homes that can be operated in a way that is economically sustainable in the context of social housing. This means that investments must in principle be funded from the income from rents with an acceptable price level for this category of housing.

The above housing costs were determined in this study in the following way.

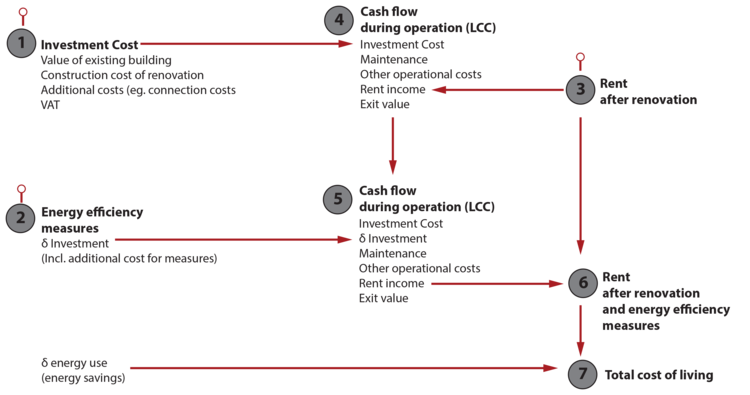

- The investment costs of major renovations were first determined without specific energy-saving measures. In this study the investment costs were defined according to the Dutch standard NEN 2699 as the value in use of the existing building + the construction costs of the renovation + the additional costs such as fees, connection costs and municipal levies + VAT [i]).

The construction costs of all renovation measures were estimated on the basis of EcoQuaestor's cost database [ii]). As a result, the cost level of the budgets is consistent with Dutch building practice. - Next, the investment costs of specific energy-saving measures (and other measures specifically aimed at sustainability) were determined. Of course, the effect of these measures on the energy use in the dwellings was also determined.

- The rent for the apartments (after renovation without specific energy-saving measures) was determined in accordance with the ‘Appropriate allocation’ scheme under the 2015 Housing Act [iii]).

- The investment (from step 1) was then included in a cash flow survey of operating costs and benefits in accordance with the LCC model of the NEN 2699 standard. In this survey, the present values of maintenance, management costs and other property expenses were included in the form of a fixed amount per property at a cost level that is typical for the sector.

On the revenue side of the balance sheet, the present value of 30 years of rental income (from step 3) was set (assuming that 30 years is the exploitation period for an apartment in the social housing sector).

In a sub-study, the realistic assumptions for the IRR and the exit value of the apartments were determined on the basis of historical data. We say ‘realistic’ in the sense that a housing corporation will be able to exploit the apartments in a financially sound manner for another 30 years after an intervention at this level of investment.

- Next, the extra investment costs of the specific measures (from step 2) were included in the cash flow survey (from step 4) and the present value of the rental income was adjusted in order to close the balance again.

- The increase in monthly rent was then determined on the basis of the figures from step 5.

- In step 7, an estimated average amount of energy costs was added to the rent (from step 3).

- Finally, the housing costs of deep renovation including the specific energy saving measures were determined. To this end, the rent from step 6 was increased by the energy costs from step 2.

The overall housing cost was presented to the residents, together with the respective renovation solution, in order to facilitate and inform their choices and preferences.

[i] NEN 2699:2017 standard

[ii] EcoQuaestor

[iii] Kennisbank Woningwet 2015